17 March 2025

general

When you save into an account that pays interest, you can expect to start seeing your money grow. Similarly, if you invest in the stock market, you likely do so in order to grow your wealth through the power of investment returns.

Compounding can be powerful for your savings and investments and lead to far greater gains than you’d initially expect. Generally speaking, there are two types of compounding:

Essentially, compound interest is the magic of earning money not just on your initial capital, but on the previously accumulated interest or returns. In fact, Albert Einstein once famously said: “Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.”

While compounding can be powerful, it may not feel like anything is happening at first. This is because it can take some time to see results.

However, there will likely come a point where your growth begins to accelerate and your total returns start to outpace the amount you have personally saved or invested. This is known as the “compound interest tipping point” and it’s where you are most likely to see advanced growth.

Here's what you need to know about the different stages of compound growth and how to identify the factors that influence when this tipping point occurs. And, perhaps even more importantly, let’s explore what this could ultimately mean for your saving and investment journey.

Compound interest starts with a slow progression but can swiftly accelerate

Consider the tipping point as a snowball rolling down a hill. Initially, growth may be gradual as the ball accumulates a small amount of snow. However, as the size of the ball increases, so too does its capacity to pick up more snow.

This typically leads to fast exponential growth in the snowball and mirrors the way compound interest or investment returns are generated.

The initial stage of investment growth is often slow. While you are generating returns, they may appear relatively small in comparison to the principal investment. Similarly, interest payments on cash could be as little as a few pence a day at first. However, as time progresses, the compounding effect takes hold, and you will likely begin to see greater performance.

Keep in mind that the tipping point is not a fixed date or a specific percentage of returns but rather a shift in the rate of growth. This may be based on how much you initially put in, time horizons, and the frequency of your contributions.

Patience and regular contributions could help grow your wealth

Several factors can influence your money’s tipping point and affect not only what you could earn but when your returns might begin to accelerate. These are:

Rate of return

When it comes to your investments, the rate of return is simply the percentage gain or loss you make on your money over a specific period. It’s a way to measure how well your investment has performed.

Think of it like this:

You buy a stock for £100 and it rises in price. Now it’s worth £110. Your profit is £10.

To work out your exact rate of return, divide your profit by your initial investment and multiply by 100. Here, your rate of return would be (10 / 100) x 100 = 10.

This means your rate of return on your initial investment is 10%. The higher your returns, the more power your money has to grow. Of course, to achieve the compounding effect, you would need to reinvest your returns rather than taking them as income, such as through dividends or fund payments.

The same theory applies to cash accounts that provide a fixed rate of interest. In this case, the compound interest you’ll receive is predictable and normally shielded from losses. However, inflation can erode your investment returns by reducing your purchasing power.

For example, if your investment grows by 5% but inflation is 3%, your real return is 2%.

Time horizons

Time is a crucial element in the compounding equation.

Again, imagine you’re investing a portion of your wealth. A longer investment time frame typically allows more time for any returns to compound. While the tipping point may be further along the line with a longer time horizon, the returns could be greater.

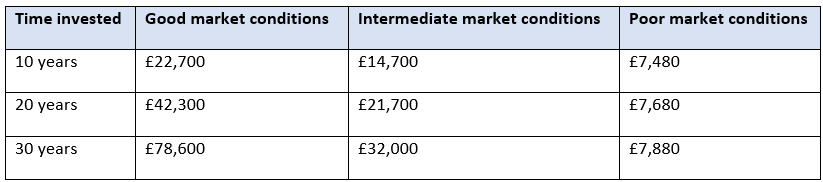

Consider the below as an example of how your returns could change based on the time you remain invested. For the below illustration, assume you initially invested £10,000, made no monthly contributions, and opted for a medium level of risk.

Source: HSBC

As you can see, remaining invested for longer is likely to generate higher returns, even if you don’t contribute anything each month. In this example, your initial lump sum will have more than doubled after 20 years in intermediate market conditions.

Here, your returns now match or exceed your initial investment, meaning your wealth has reached the tipping point.

What’s more, if you were to contribute frequently in addition to your initial £10,000 investment, you could see your returns grow exponentially and potentially reach the tipping point more quickly.

Contribution frequency

Regular contributions to a savings or investing account tend to amplify the compounding effect by consistently increasing the principal amount on which interest is calculated or gains are made.

For this reason, more frequent contributions could accelerate the journey to the tipping point. This can be true for both investments and cash savings that pay interest.

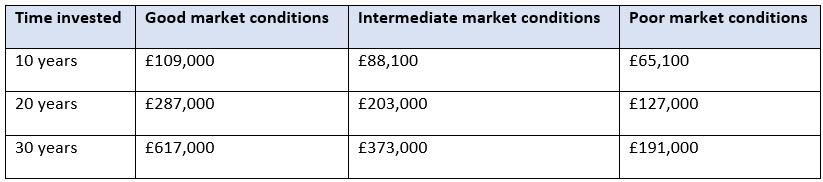

For this next illustration, we’ll take the initial investment of £10,000 but add monthly payments of £500.

Source: HSBC

Comparing this table to the one above demonstrates how much more growth you could see with regular contributions. You can also see how both rates of return and time horizons play a role in the outcome of your investment.

Consider that your initial investment along with your monthly contributions add up to around £70,000.

Here, your compound interest tipping point is likely occurring at around 15 years in intermediate market conditions. This is because, by year 20, you have reached £203,000, which is more than double your initial investment and monthly contributions. In good market conditions, this date may arrive even sooner.

Keep in mind that the “healthier” your portfolio is, the more likely you are to see success. This means exploring how to diversify your portfolio to minimise the effects of poor market conditions and finding ways to balance risk against returns.

Taking the example of earning interest on your cash, the same principle applies, but cash might grow more slowly than investments over the long term. On a more positive note, though, while investments can have a degree of volatility, cash is very low-risk. Balancing both is usually the most appropriate course of action.

Get in touch

To learn more about how to make your money work harder for you, talk to us today.

Email enquiries@jesellars.co.uk or call 01934 875 919 to find out more about how we can help.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.